From wildfires and floods to scorching heatwaves, the consequences of climate change are becoming more pronounced, and as we enter the peak shipping season, businesses are scrambling to prepare for what is predicted to be one of the most disruptive storm seasons in recent memory.

So far in 2024 supply chain disruptions caused by extreme weather are estimated to have cost companies billions of pounds, and the storm season is far from over. Hurricanes, wildfires, and floods have already stretched global supply lines thin, and the arrival of storms like Typhoon Bebinca, which threatened Shanghai this week, adds a fresh layer of concern.

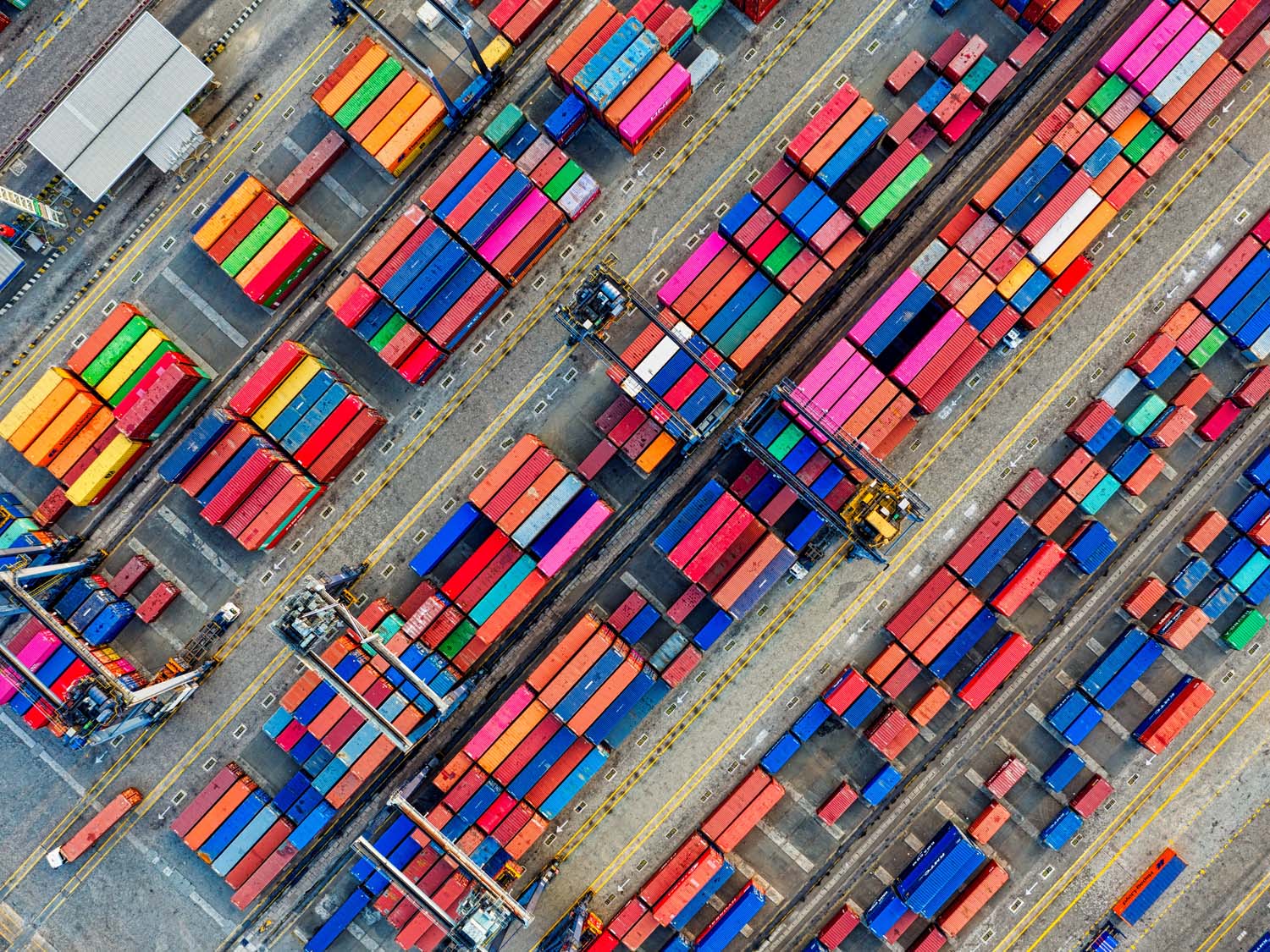

Increased visibility allows managers to pinpoint disruptions and adjust supply chains accordingly, and the key to weathering these events lies in preparation. Shippers are diversifying their carrier bases and building inventory buffers to keep goods moving in the face of challenges. Strategic planning, such as maintaining safety stock for high-demand items, has become essential in managing supply chain risks.

The heightened storm season comes as companies are already reeling from the effects of wildfires in California and Australia, as well as floods that have caused widespread damage to transportation networks in Asia.

While technology and data-driven insights have made supply chains more resilient, this year’s relentless barrage of natural disasters is proving particularly difficult to navigate. While technology can help predict and respond to the impact of storms, it is only effective when paired with clear communication and regular updates on shipments.

The threat posed by Typhoon Bebinca is yet another reminder of the supply chain vulnerabilities that remain, with Shanghai closing ports, cancelling, and halting transportation links to ensure safety. With more storms likely in the coming months, companies must remain agile and vigilant, ready to adapt to further disruptions.

The need for resilience and adaptability is more pressing than ever, as companies navigate the challenges ahead. This season may prove to be one of the toughest in recent memory, but for those prepared, there are still opportunities to maintain operational continuity in the face of adversity.

Extreme weather events consistently highlight the vulnerability of supply chains and the importance of robust contingency plans and marine insurance to protect against risk.

We have been maintaining supply chain resilience in the face of unforeseen challenges for decades. To learn how we can develop and support your supply chain resilience EMAIL our Chief Commercial Officer, Andy Smith.