New research by the British Chambers of Commerce (BCC) has found that over half of importing manufacturers and retailers (53%) have been impacted by the disruption to shipping caused by the Red Sea crisis, with over half of exporters (55%) also experiencing increased costs and delays.

The issues highlighted by responding firms included increased costs of up to 300% for shipping, with transit delays adding up to three to four weeks to delivery times. Knock-on effects include cashflow difficulties and component shortages on production lines.

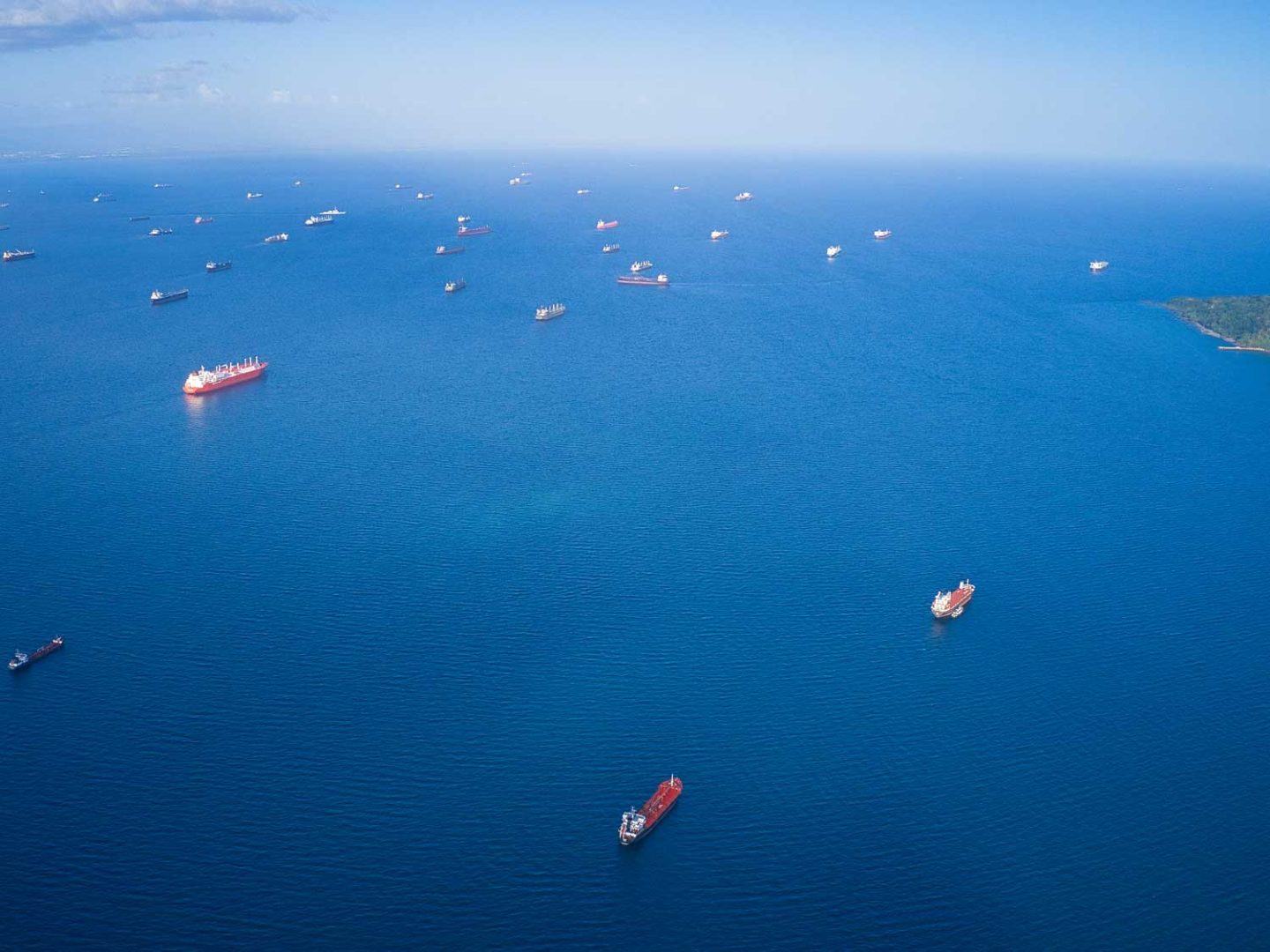

With a record-high new container ship order-book and constrained consumer demand in many markets, the container shipping sector has had ample spare capacity to respond to the challenge of diverting vessels around the southern top of Africa.

The Red Sea transit to the Suez Canal is the fastest sea route between Asia and Europe, but all the major container shipping lines have diverted vessels to the much longer route around Africa’s Cape of Good Hope, increasing costs and creating delays.

Recent ONS data suggest the ‘Red Sea effect’ has yet to filter through to the UK economy, with inflation holding steady in January. However, the longer the current situation persists the more likely it is that the cost pressures will start to build, with some sectors of the economy more exposed than others.

The UK economy saw a drop in its total goods exports for 2023, and with global demand weak, the BCC want the Government to look at providing support in the March Budget, including the establishment of an Exports Council to hone the UK’s trade strategy and a review of government funding for export support.

Week 12 of the Red Sea crisis

The war in Gaza, which according to the Houthis is the reason for their attacks on commercial shipping, shows no sign of abating and on Monday the Rubymar finally sank, the first total loss in the Houthis campaign.

Vessel schedule reliability data for January 2024 confirmed that global reliability dropped sharply due to the Red Sea impact and only slightly more than half of vessels arrived on time, compared to pre-pandemic normality of 70-80%.

Geopolitical risk

The wars in the Middle East and Ukraine are threatening flows of grain, oil and consumer goods, with climate change disrupting the Panama Canal and growing geopolitical tensions are making international supply chains ever more complex.

The World Economic Forum’s Global Risks Report (GRPS) for 2024 highlights how geopolitical tensions in multiple regions is contributing to an unstable global order, eroding trust and security.

GRPS 2024 results highlight a predominantly negative outlook for the world over the next two years, that is expected to worsen over the next decade, with supply chain disruption ranked 19th of severe global risks in the short term (2 years) and 25th for the long term (10 years).

Over the next two years, attention is likely to be focused on the war in Ukraine, the Israel-Gaza conflict and tensions over Taiwan, with any escalation likely to disrupt global supply chains.

All three areas stand at a geopolitical crossroads, where major powers have vested interests: oil and trade routes in the Middle East, stability and the balance of power in Eastern Europe, and advanced technological supply chains in East Asia.

If you have any questions or concerns about the impact of the Suez situation on your Asia supply chain, or would like to discuss its wider global implications, please EMAIL our Chief Commercial Officer, Andy Smith.