Metro continues to actively support the development and adoption of emerging technology, across the shipping industry, by participating in the successful testing of new e-FIATA Bill of Lading (eFBL) standard, with FIATA , the trade association for 40,000 freight forwarding and logistics firms in 150 countries.

The COVID19 pandemic has highlighted the urgent need for adoption of the digital version of one of the most important trade documents – the bill of lading.

At ports and terminals around the world, goods cannot be released because the paper bill of lading is not there due to border restrictions, changes to the cargo’s routing, or people cannot physically stamp the document.

The ongoing disruption to trade, transport and the movement of documents, means that the digitisation of physical shipping documents is becoming much more significant

Several solution providers and carriers have offered proprietary versions of eBLs but the lack of standardisation has prevented large-scale adoption.

Metro’s tech experts work with the United Nations Centre for Trade Facilitation and Electronic Business (UN/CEFACT), to harmonise trade documents and the exchange of information in the supply chain

In 2021, FIATA will release its eFBL standard, which is based on the UN / CEFACT Multimodal Transport Reference Data Model, to ensure interoperability with other standards and most systems.

“From a trust perspective we definitely see value in the document audit trail and the possibility for stakeholders to check the validity of documents.”

Simon George, Technical Solutions Director, Metro Shipping

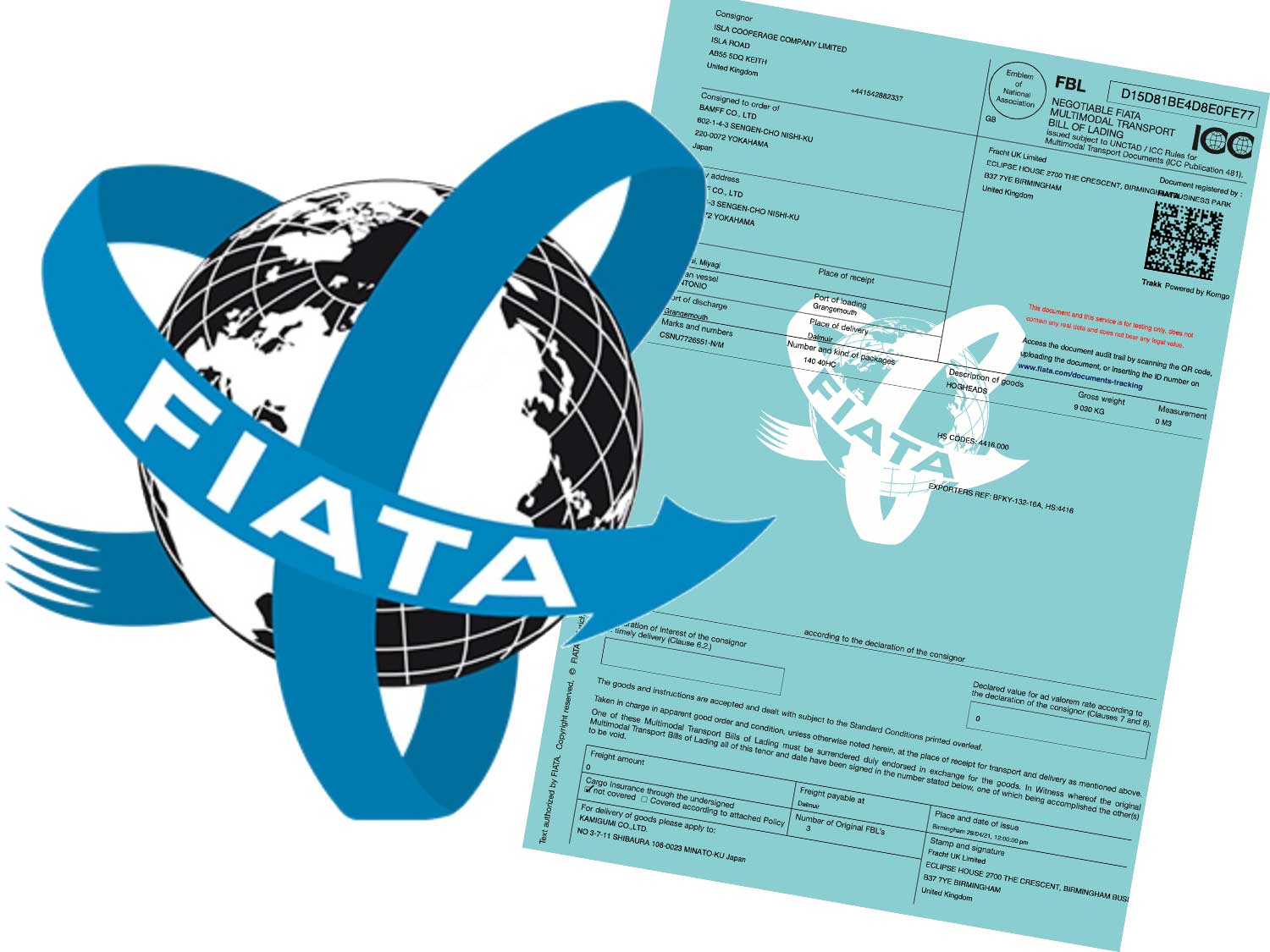

Earlier this month FIATA’s eFBL was tested by Metro, other freight-forwarding companies and software providers, as part of a proof of concept, aiming to make the open source standard available to all.

As part of the concept testing, Metro’s operations system generated a document that went electronically to FIATA’s servers, made an entry containing ‘issue date’ and ‘issued by’ as well as the document itself, which then sent back a FIATA bill of Lading directly into our operations system.

FIATA really appreciate Metro’s assistance, in testing the electronic FIATA Bill of Lading issuance, sharing and verification processes. The detailed feedback will ensure our eFBL solution does answer to the needs of members around the world.

Lucelia Tinembart, Digital Projects Officer, FIATA

FIATA is going even further by testing a tracking solution for its documents, which will allow full traceability, through a unique QR code and number attached to each document. This will enable all parties interacting with an eFBL to verify the validity of the document, the integrity of its content, as well as the identity of its issuer, by scanning the QR code or uploading the PDF on FIATA’s website.

Full implementation is planned to start in Q3 / 2021.

Metro believe that Blockchain, machine-learning and emerging technologies are the future of international trade. That’s why we work with UN/CEFACT and FIATA: to harmonise the exchange of information in the supply chain; and develop digital capability with critical documents like eBL’s.

For specific information, or to discuss how our technology could support your supply chain, please contact Simon George our Technical Solutions Director.