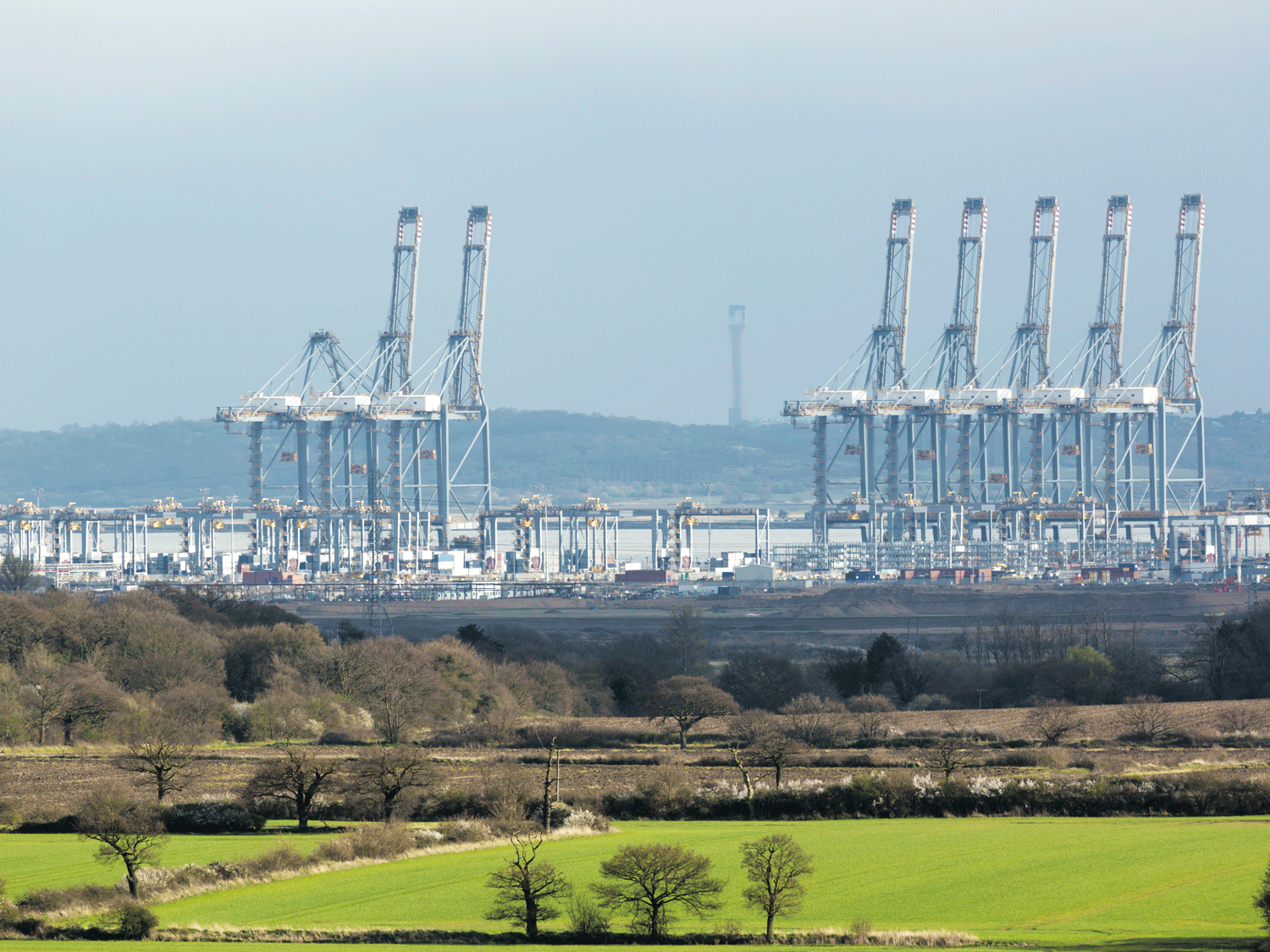

DP World has opened an 11.5 acre container park near Southampton, to increase storage capacity during the peak pre-Christmas season and work has begun on a fourth berth at London Gateway container port, to increase supply chain resilience and create more capacity for the world’s largest vessels.

The new park at Southampton will be able to hold additional empty containers and reduce stack sizes at the nearby container port, a critical factor in keeping supply chains moving at a time when dwell times at terminals across the UK have increased.

The new £3m empty park is part of DP World’s £40m investment this year at Britain’s second largest container terminal - designed to take it up to the next level as a smart logistics hub - which will provide 25% more storage capacity at Southampton and enable the port to maintain productivity and service levels for the vital next few months.

Southampton has already benefitted this year from the dredging and widening of berths to ensure continued accommodation of the world’s biggest ships and a £1.5m extension of a quay crane rail by 120 metres to ensure that the world’s biggest cranes can service the entire terminal and receive the largest container vessels that are operating today and in the foreseeable future.

In the first half of 2021, a record volume of cargo was handled at Southampton, with throughput of 995,000 TEU, while London Gateway saw record throughput of 888,000 TEU, a more than 23% increase on the previous best performance. Impressive although not without some pain during the process.

Southampton and London Gateway have both been awarded freeport status as part of Solent Freeport and Thames Freeport respectively.

The new London Gateway berth is part of a £300M investment by DP World, to support Thames Freeport and will raise capacity by a third. Completion of the new berth will coincide with the delivery of a new wave of 24,000 TEU vessels in 2023/2024, which will undoubtedly be operated between Asia and Europe.

Along with the Port of Tilbury and Ford’s Dagenham plant, London Gateway will form part of Thames Freeport after being awarded ‘freeport’ status by the Government earlier this year, as a stimulus to both the local and national economy and global trade initiative.

With 40 commercial ports in the UK and hundreds across continental Europe to choose from, we select the optimum mix of cost and operationally effective port-pairs, to complete your transit in the shortest possible time.