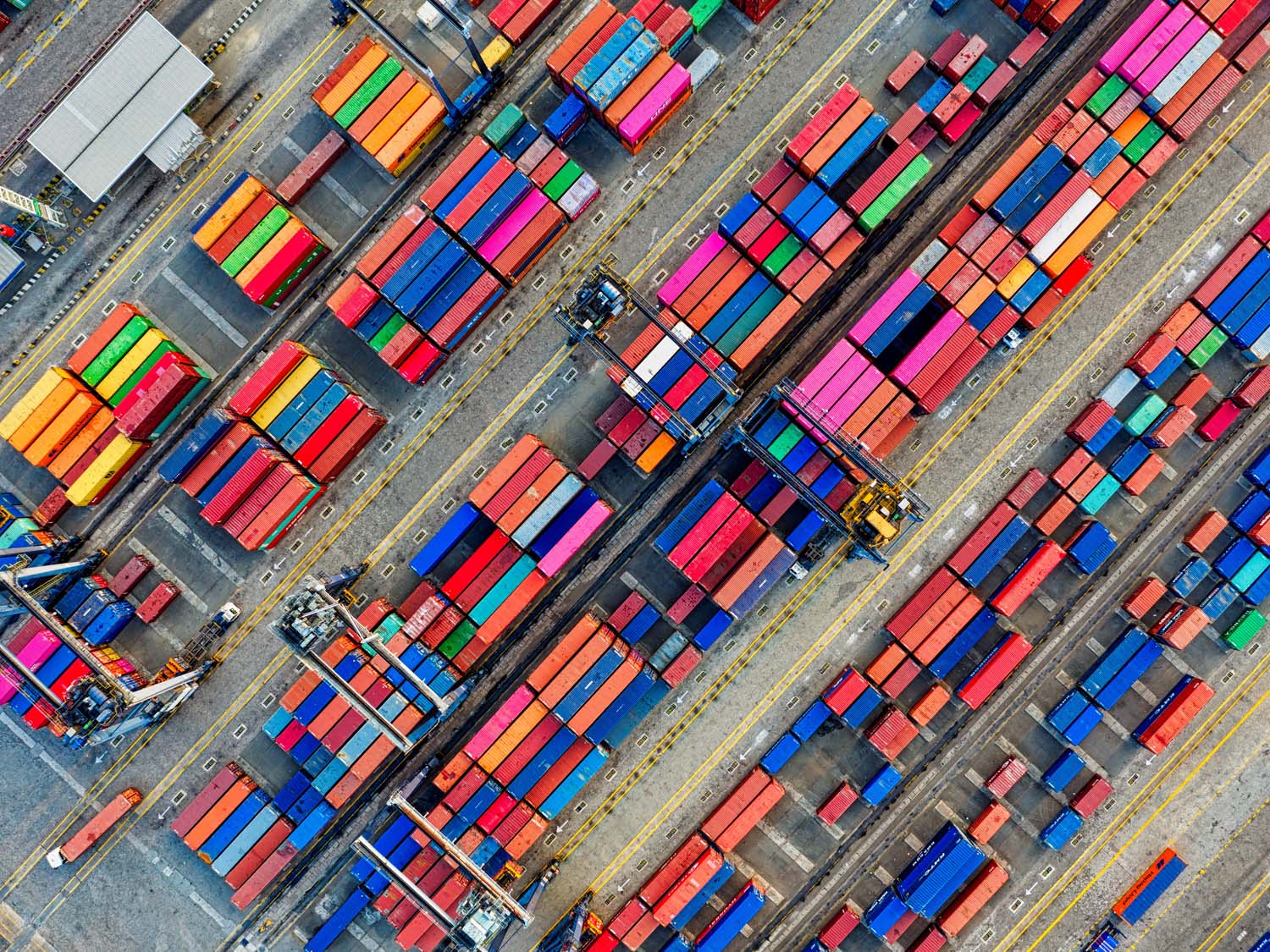

If travel for the Lunar New Year holidays increases COVID transmission, we will see large numbers of infected workers having to quarantine, which will delay their return to work and factories, hauliers, terminals and ports that would traditionally restart operations by mid-February could be shut significantly longer, with export and supply chain delays.

This Sunday, the 22nd January marks the start of the Lunar New Year and is the trigger for Chongqing-Chunyun, the Chinese New Year Migration, which is the largest annual human migration on earth, with hundreds of millions of people, working out of their hometowns, hurrying home to be with their families for the two-week holiday.

Factories and most other parts of Chinese society close down for the duration of the holiday (which is based on the lunar cycle), causing a pause in exports leaving the country, which is why traditionally we would see a spike in freight volumes - and particularly - air in the run up to CNY.

China’s economic growth of 3% in 2022 was the weakest since 1976, prompting the abrupt lifting of China’s strict zero-Covid policy in December. Unforeseen by many although encouraged for a long time.

With the recent rapid dropping of COVID restrictions across China, workers are more free to travel than they have been since 2020, which has led, predictably, to a surge in infections and with high levels of COVID in travellers leaving China for business and vacation, countries including the UK have introduced testing for incoming flights from China. Restrictions haven’t just been ‘eased’, but they have been withdrawn entirely in some areas. This is rapid deployment of the new measures.

If New Year’s travel does lead to increased transmission across the country, which logic dictates it is hard to avoid - large numbers of infected workers will need to quarantine, delaying their return to work, with means that supply chain infrastructure and factories that would traditionally restart operations by mid-February could be side-lined for significantly longer, resulting in export order and shipping delays.

Some importers are still carrying plenty of inventory and may not be impacted, but for those with products that are selling well, they may get caught up in the shortfall and a scarcity of bestsellers.

At the end of December, China stopped publishing daily COVID transmission data, possibly to conceal negative information about the pandemic circulating. But shippers will probably know sooner than just about anybody, when they don’t get the deliveries they were expecting out of China.

We have seen many factories and manufacturing sites throughout China shutting early this year already, either because they were quiet, or to give workers an extended break. This has contributed further to the lull in container movements, in what should traditionally be a peak week prior to the CNY celebrations.

There is, as a consequence, a huge number of shipping line schedule changes, blanking’s, suspensions and withdrawals over coming weeks and months, that will impact on vessel departures and planning reliability in China and across Asia. As a result, it could take a long time to unwind, with return eastbound voyages in March and possibly beyond.

Economists have warned over the state of the global economy in recent months and the International Monetary Fund (IMF) has urged Beijing to continue reopening its economy.

The IMF believe that if China stay the course - and do not re-impose COVID restrictions - by mid-year or there around, they will turn into a positive contributor to average global growth.

However, the full reopening of China's borders is likely to be delayed until international restrictions against China-originated travel are dropped.

On the upside with travel restrictions from and to China being relaxed the air cargo market is likely to see benefit with belly-hold capacity returning to pre-pandemic levels, as tourists look to travel once again, on passenger flights being re-introduced on routes that have been closed and which should result in reduced air freight costs, to and from the region.

As China emerges from its COVID stasis, we have fixed price and long-term capacity agreements in place with our partner carriers, to deliver resilient, consistent and reliable supply chain solutions.

Metro’s cloud-based supply chain management platform, MVT, simplifies global trading, by making every milestone and participant in the supply chain transparent and controllable, down to individual SKU level.

To discuss how our technology could support your supply chain, please contact Simon George our Technical Solutions Director or Elliot Carlile for all options relating to current freight profile movements to and from China.