Date:

2022; Supply chain outlook

Supply chain pressures remain well above their pre-pandemic levels, but studies of worldwide supply chain constraints produced by the Federal Reserve Bank of New York suggest that pressures peaked in October 2021, raising faint hopes that global trade could start to normalise this year.

The gauge of worldwide supply chain constraints produced by the Federal Reserve is based on 27 variables, including global shipping rates and air freight costs, which dipped slightly lower in November and December, even as many countries face rising cases of the Omicron coronavirus variant and persistently high inflation.

Some analysts believe that the squeeze in certain areas will continue to ease off in the coming months, with some supply chain disruptions resolving themselves, while others may prove more persistent.

The swift reopening of the global economy caught many by surprise last year and while some sectors seem to be improving, many are still dealing with pandemic-related pressures, factory shutdowns and logistics bottlenecks.

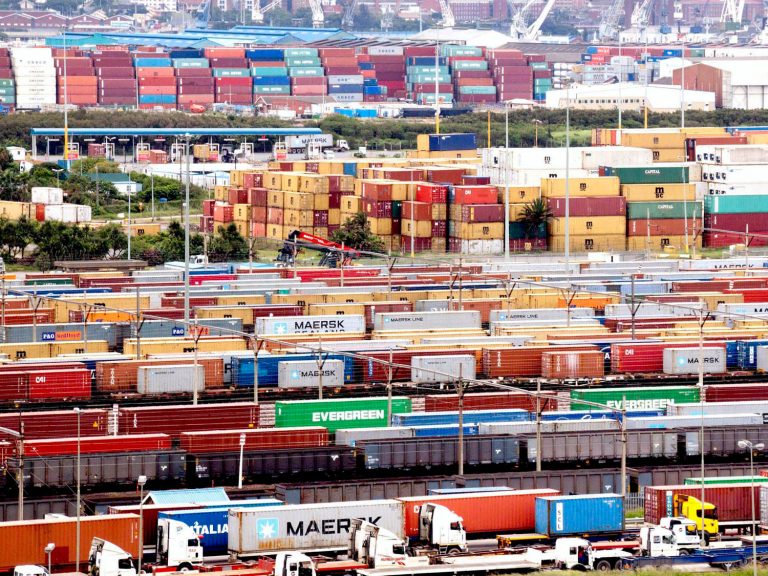

Last year was a perfect storm for supply chains, with COVID disrupting global production, at the same time as the impact of the pandemic boosted consumer demand. The Suez Canal closure and terminal closures at two of the world’s busiest container ports caused months of disruption, knocking the highly synchronised global transport system out of rhythm.

Record vessel delays clogged ports and crammed warehouses and shippers competed to secure space in aircraft and on container ships, to keep production and sales moving, while facing cash flow pressure from increasing freight rates. Inevitably, as a result, consumers began to see empty shelves, limited product availability and rising prices.

If the bottlenecks persist in Asia Europe and the US, freight costs will remain high, cargo space will be limited and shippers will continue to face delays, that could in turn fuel inflation, prompting supply chain upheavals and accelerate consolidation of shipping networks, fundamentally changing world trade.

The size of the queue of vessels lined up outside Los Angeles/Long Beach, the US gateway for Asian imports, has become a barometer of worldwide supply chain convulsions and the number of container ships waiting is at a record high.

LA/Long Beach accounts for roughly 22% of shipping capacity waiting to berth globally and if that bottleneck could be resolved, there would be enough capacity for the rest of the system.

Supply chains could prove more resilient this year, particularly if inflation hits consumer confidence and, in addition, any surplus in orders from the end-of-year holidays could help inventories replenish while outstanding orders come through.

The return of tourism, hospitality, rocketing fuel bills and higher-interest rates could all soften demand for goods, with some suggesting that shipping congestion could ease within weeks once consumers begin feeling the pinch.

Even as economists are generally optimistic about the year ahead, most indicators of supply-chain stress remain elevated above pre-coronavirus times and container shipping rates are still many times their level at the start of last year.

China’s zero-risk COVID approach remains a significant concern for supply chains this year, as any new wave of coronavirus infections, could lead to factory and port closures, which would further disrupt shipping.

Whatever challenges this year may hold we will continue to power the supply chains of our British headquartered and international customers, with our freight management and outsourcing teams and our multi-award winning MVT supply chain platform.

The MVT platform harnesses every supply chain participant, process, and milestone, to provide the real-time visibility, control and intelligence that supports resilient, flexible supply chains.

For further information on our MVT tool and to discuss how we can enhance your supply chains, please get in touch with Elliot Carlile or Simon George.